This post is a comprehensive guide about the cash flow statement.

In this guide, you will learn:

- Basic cash flow statement

- Three parts of activities

- Format and real-life examples

- How to create and use it

So let’s start from the beginning.

Chapter 1: Cash Flow Statement Basics

In this chapter, I cover basic things, such as what a cash flow statement is and why it’s important.

This chapter will help you gain basic information.

What is a Cash Flow Statement

A cash flow statement is one of the three main financial reports detailing a company’s finances, published by the organisation under GAAP rules.

These main three financial reports are:

- Income statement

- Balance sheet

- Cash flow statement

To understand this concept deeply, you should have an idea about all three reports.

Income Statement:

This report shows the revenue of the company and all its expenses.

The income statement starts with net sales and ends with net income by subtracting all the expenses.

Balance Sheet:

This financial report works as its name sounds.

It includes all of the company’s assets, liabilities, and shareholders’ equity, encompassing both short-term and long-term aspects.

Cash Flow Statement:

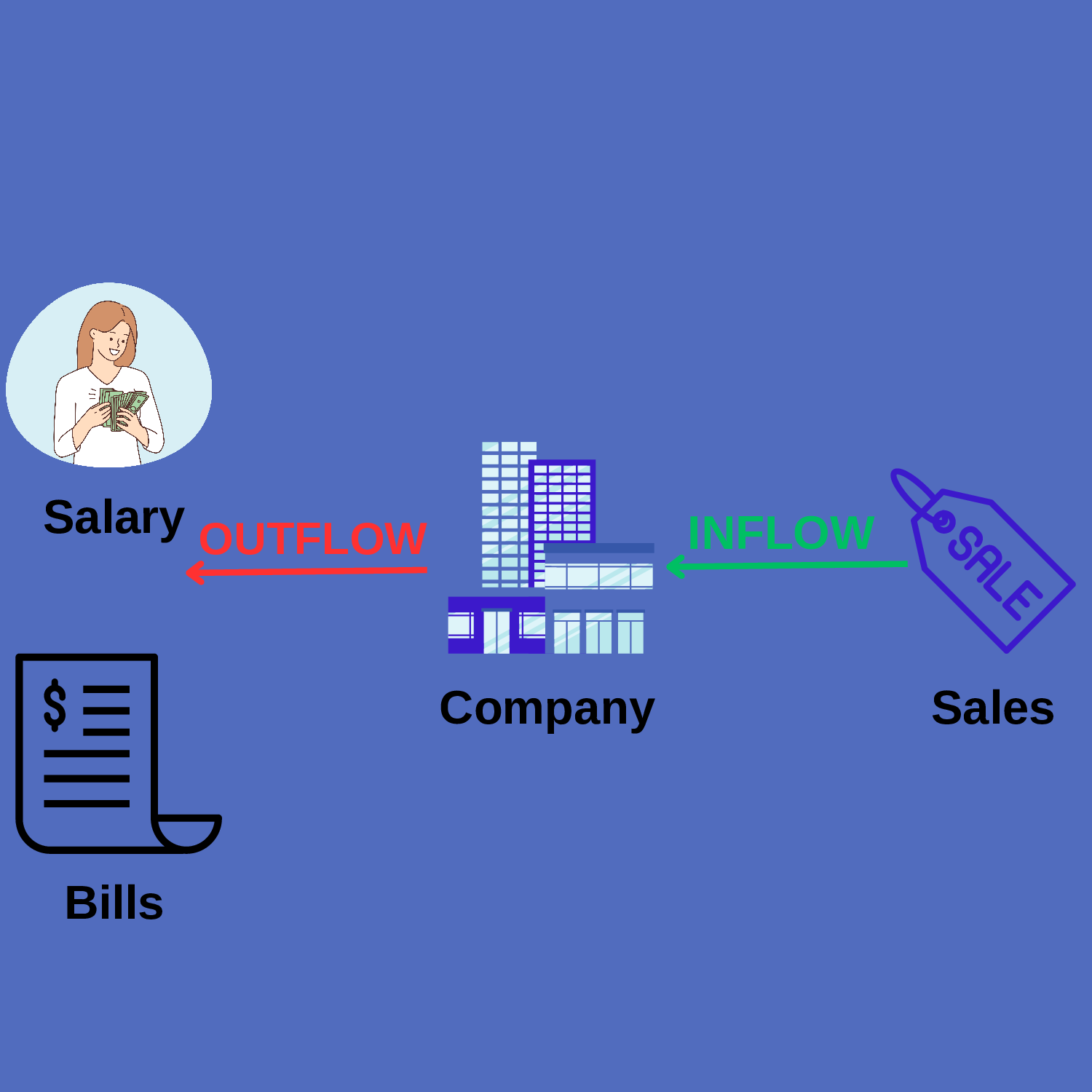

This statement tracks the inflow (flowing inward) and outflow (flowing outward) of the company’s money during an accounting period.

It includes all sources where cash comes in and where cash goes out.

For example,

a mobile company gets cash by selling a mobile, so it is included as cash inflow.

On the other hand, if the company pays a salary to its employees, it is included as cash outflow.

Why is Cash Flow Important

“Cash flow is the lifeblood of the business,” and this statement is very accurate.

The cash flow statement shows professionals and investors the actual position of the company.

More specifically, it indicates how much money the firm has.

It’s essential to note that profit (income) and cash are different.

If you sell a product worth $10,000, it doesn’t mean you have $10,000 in cash on hand because some customers may buy products on credit, and payments may be delayed.

Having data of cash is necessary for both investors and management.

The reason is they are getting answers from the cash flow statement, such as:

- Is the company facing any issues?

- Does it have enough money to pay debts?

- Can it absorb financial crises?

- Does it have the capability to capture suddenly rising opportunities?

Management makes decisions to improve the company’s health, while investors make decisions to invest money based on those answers.

Now, let’s move on to the next chapter.

Chapter 2: Breakdown of the Cash Flow Statement

This chapter delves into every part of the cash flow statement and explains each component with examples.

You will learn the format of the statement, the three types of business activities, and much more.

Format of the Statement

Under GAAP rules, creating a cash flow statement is not only mandatory but organisations should follow the same format.

While some items may vary across industries, the format should remain the same.

For example, a company providing streaming services may have different components compared to a company selling electronic products.

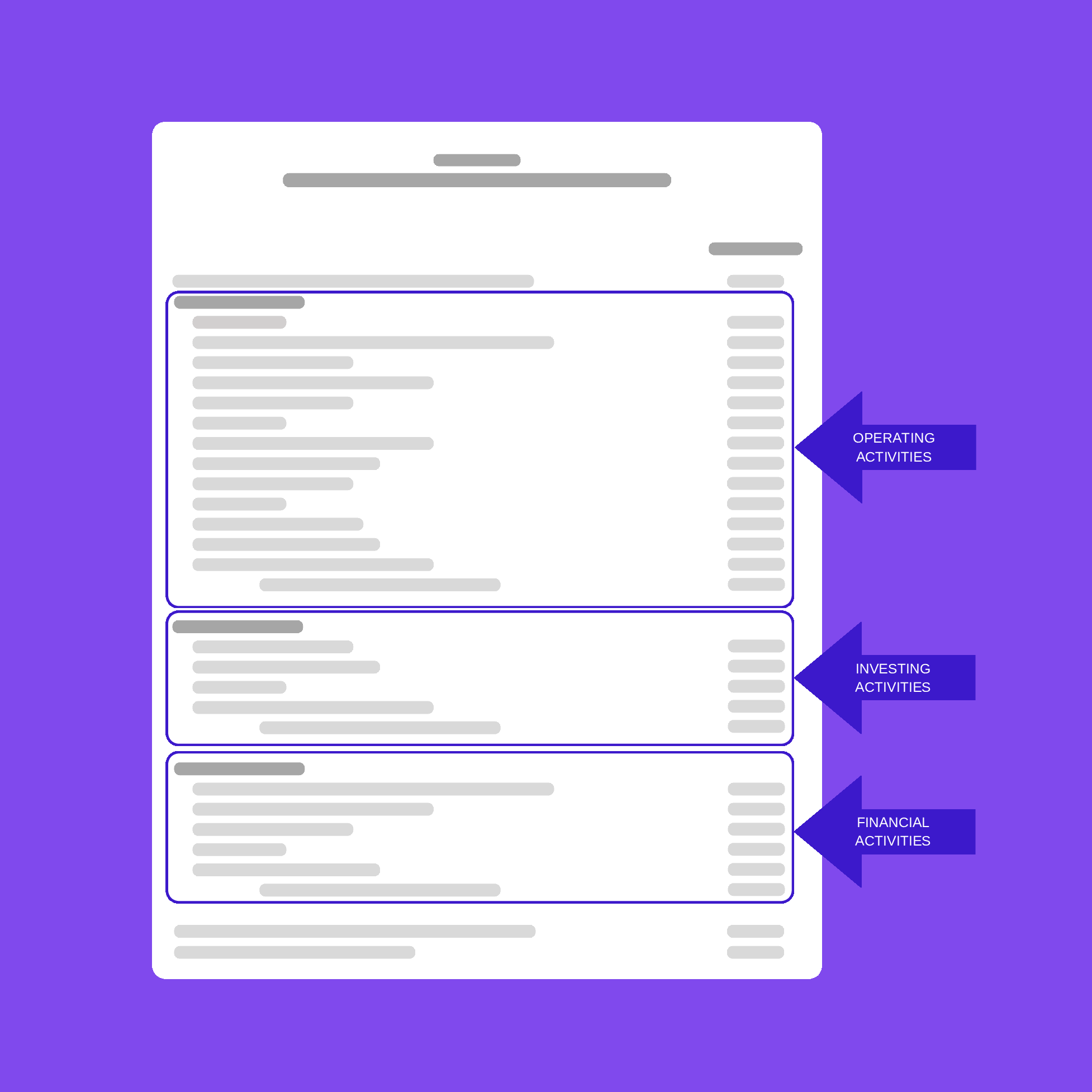

The cash flow statement contains three types of business activities, presented in chronological order according to the format.

Three activities are:

- Operating activities

- Investing activities

- Financing activities

Except that, Before operating activities and after financing activities, the statement has certain components.

Top of the statement

To understand the cash flow statement, it’s essential to grasp the full format.

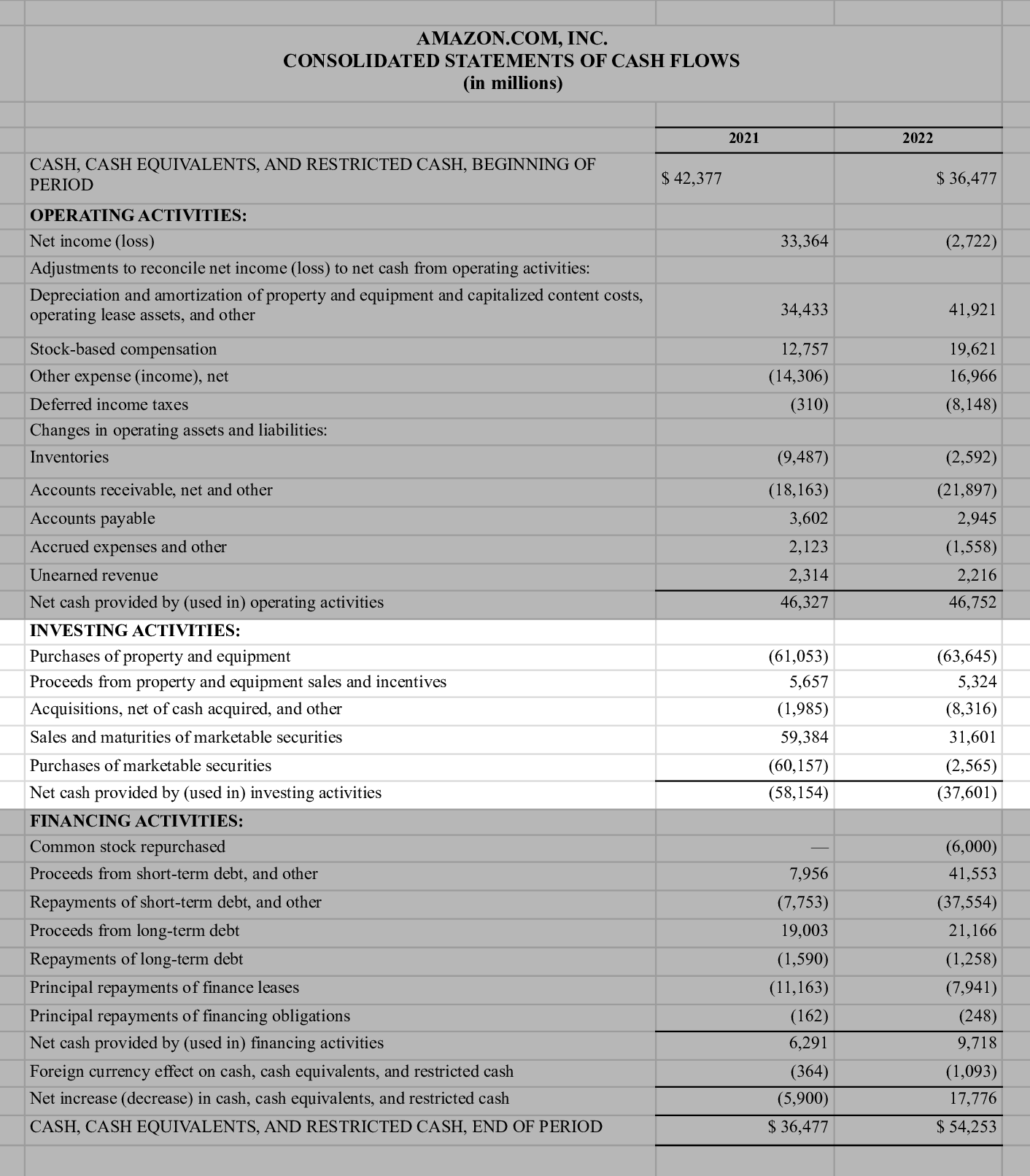

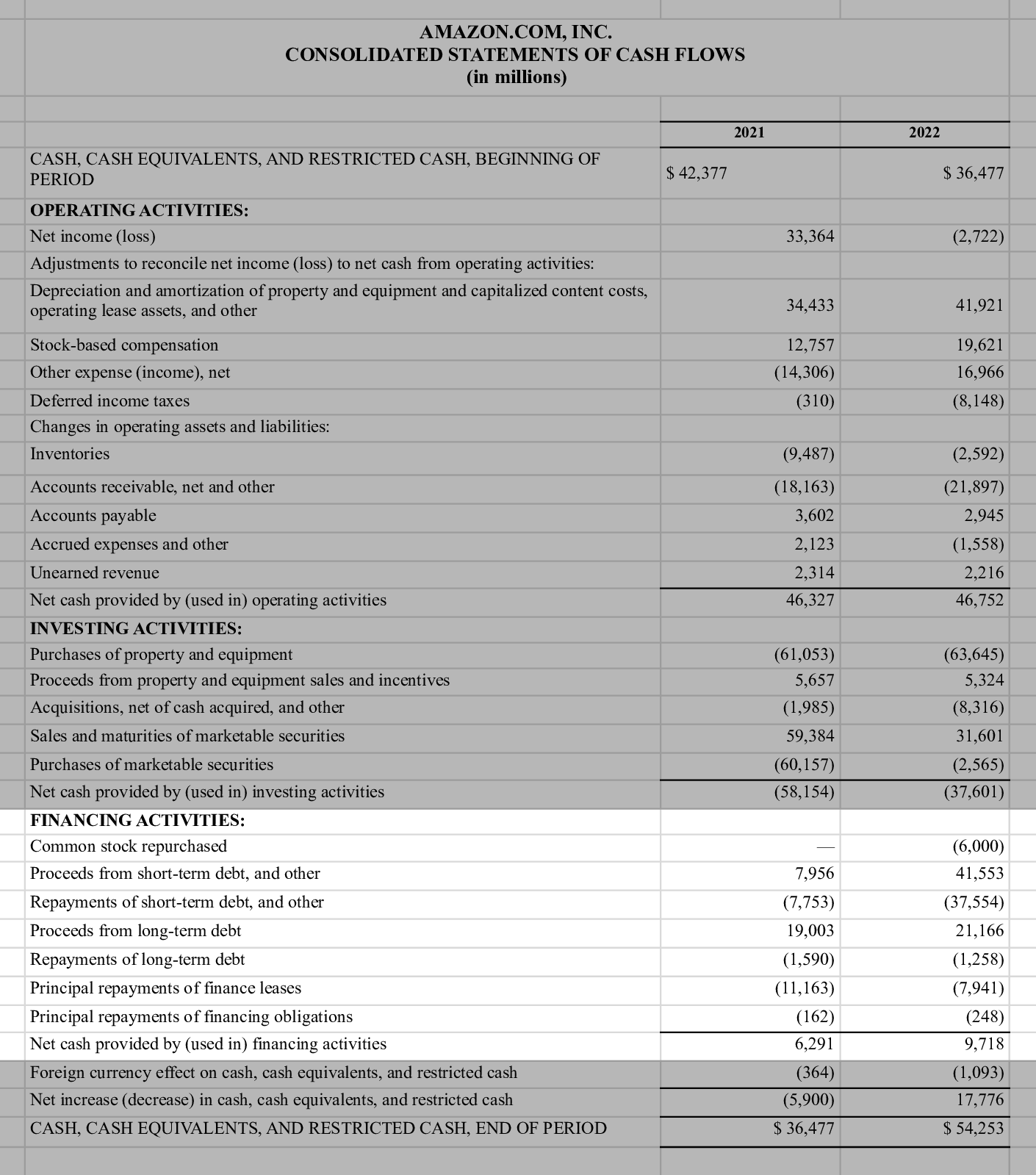

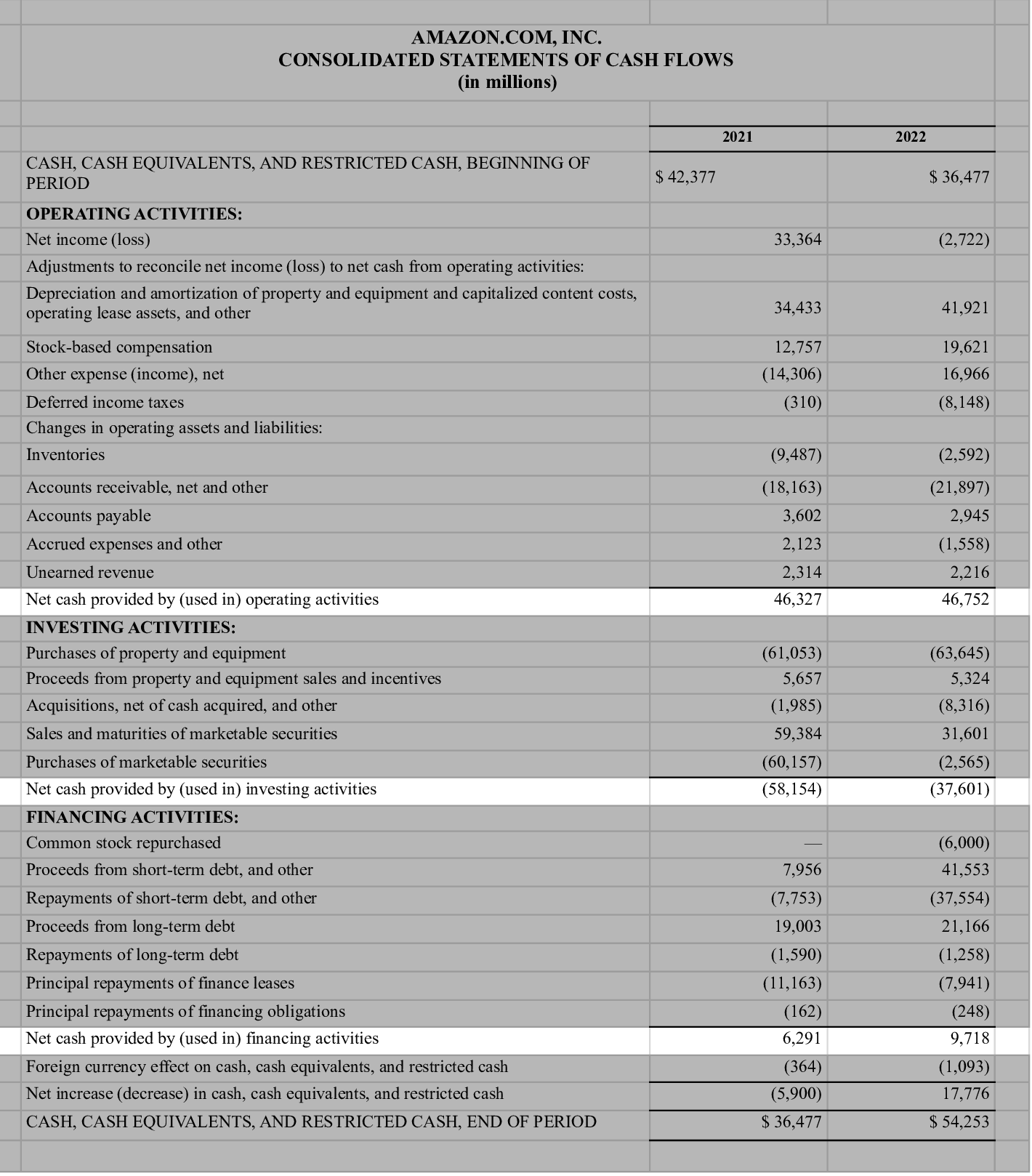

The company’s name is written at the top and followed by the line “Consolidated Statement of Cash Flow.”

In the last, Numbers are often presented in millions for clarity.

especially for large organisations like Amazon and Apple, which deal in transactions worth millions to billions.

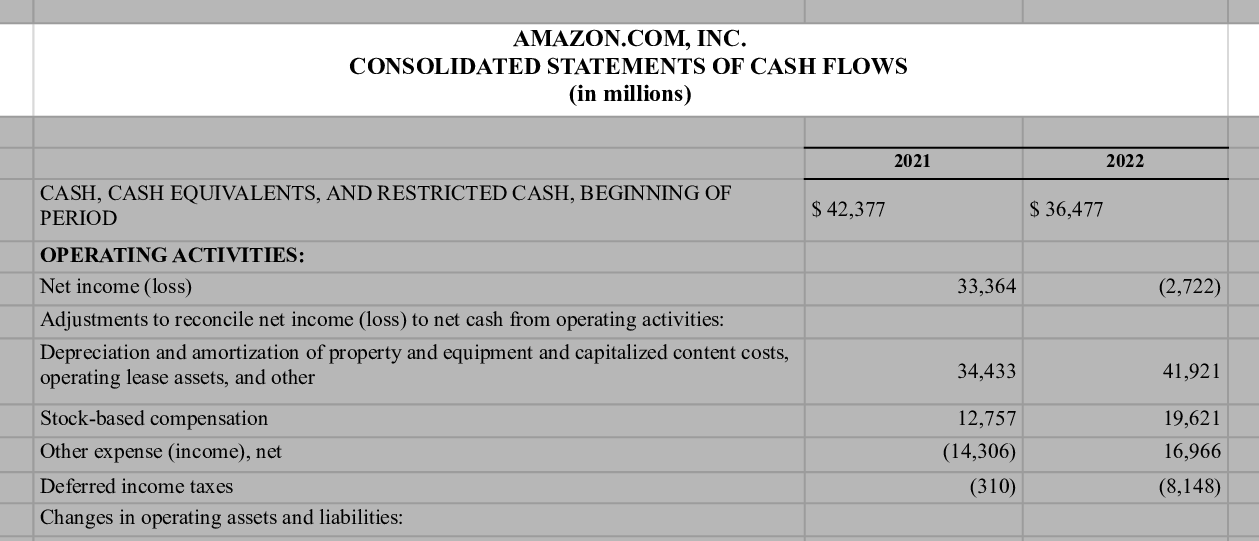

Moving on, the first component of the statement is the opening balance or you can call it cash and cash equivalents.

This figure shows how much cash the firm had in the last accounting period.

It signifies the closing balance of the previous period as the opening balance of the next.

For example,

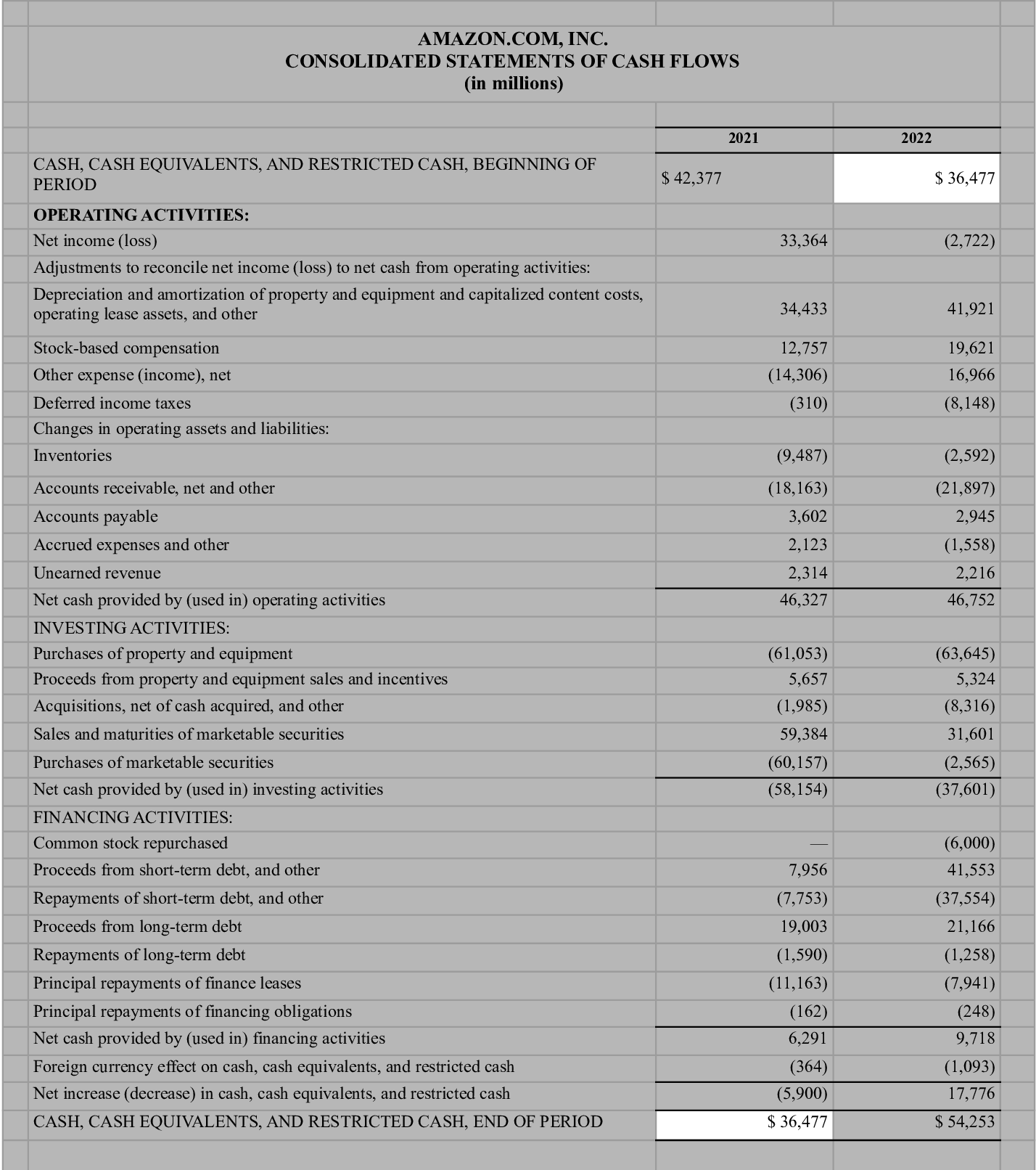

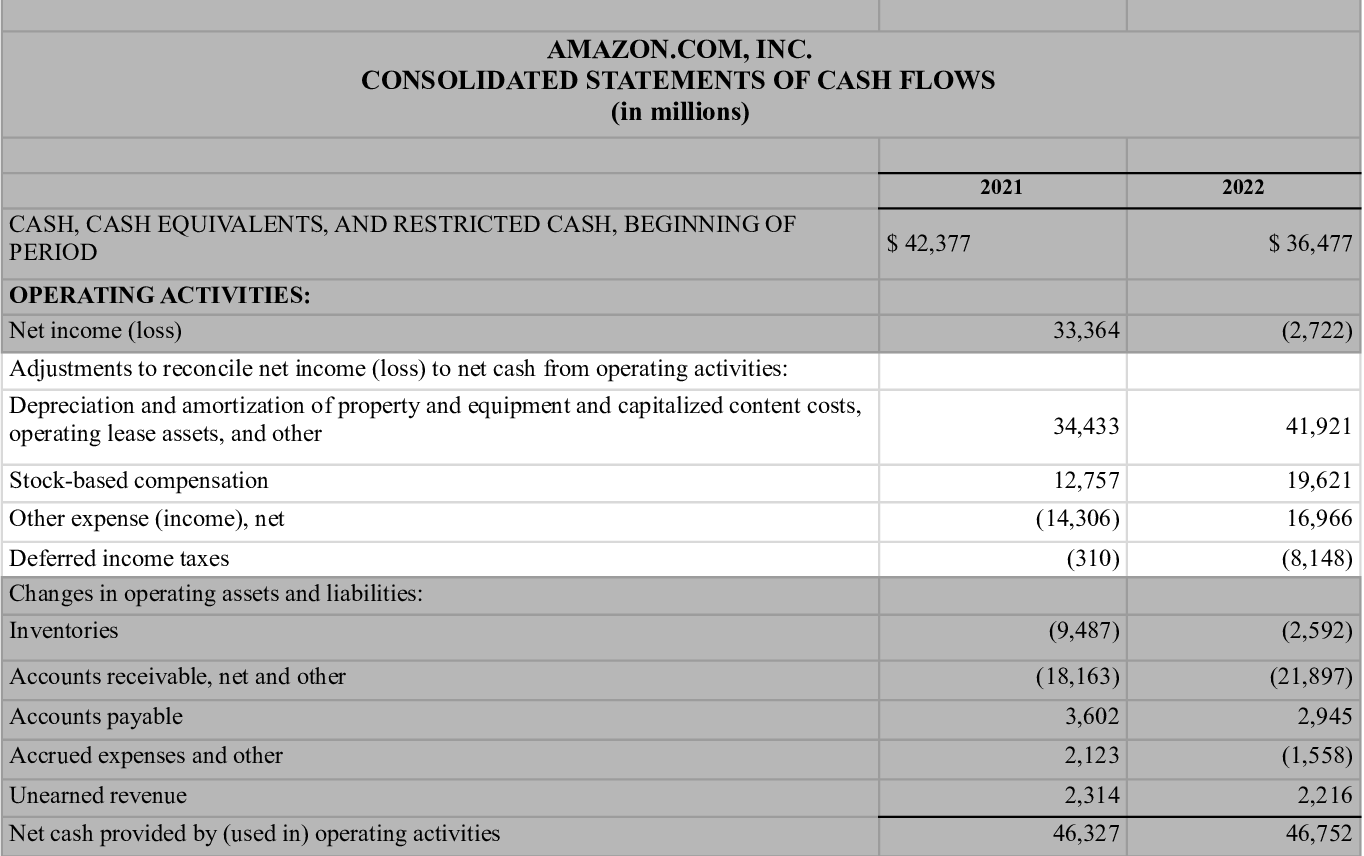

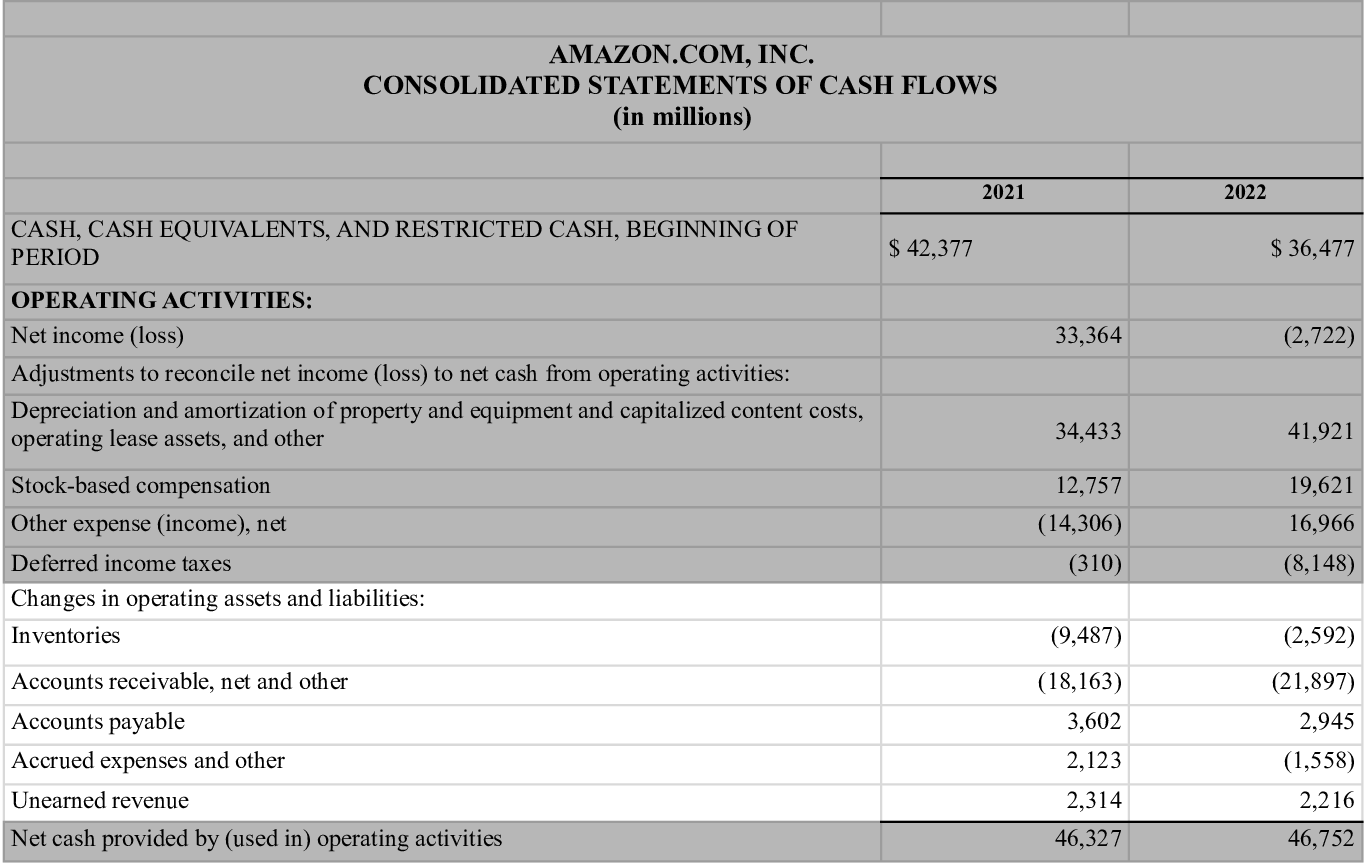

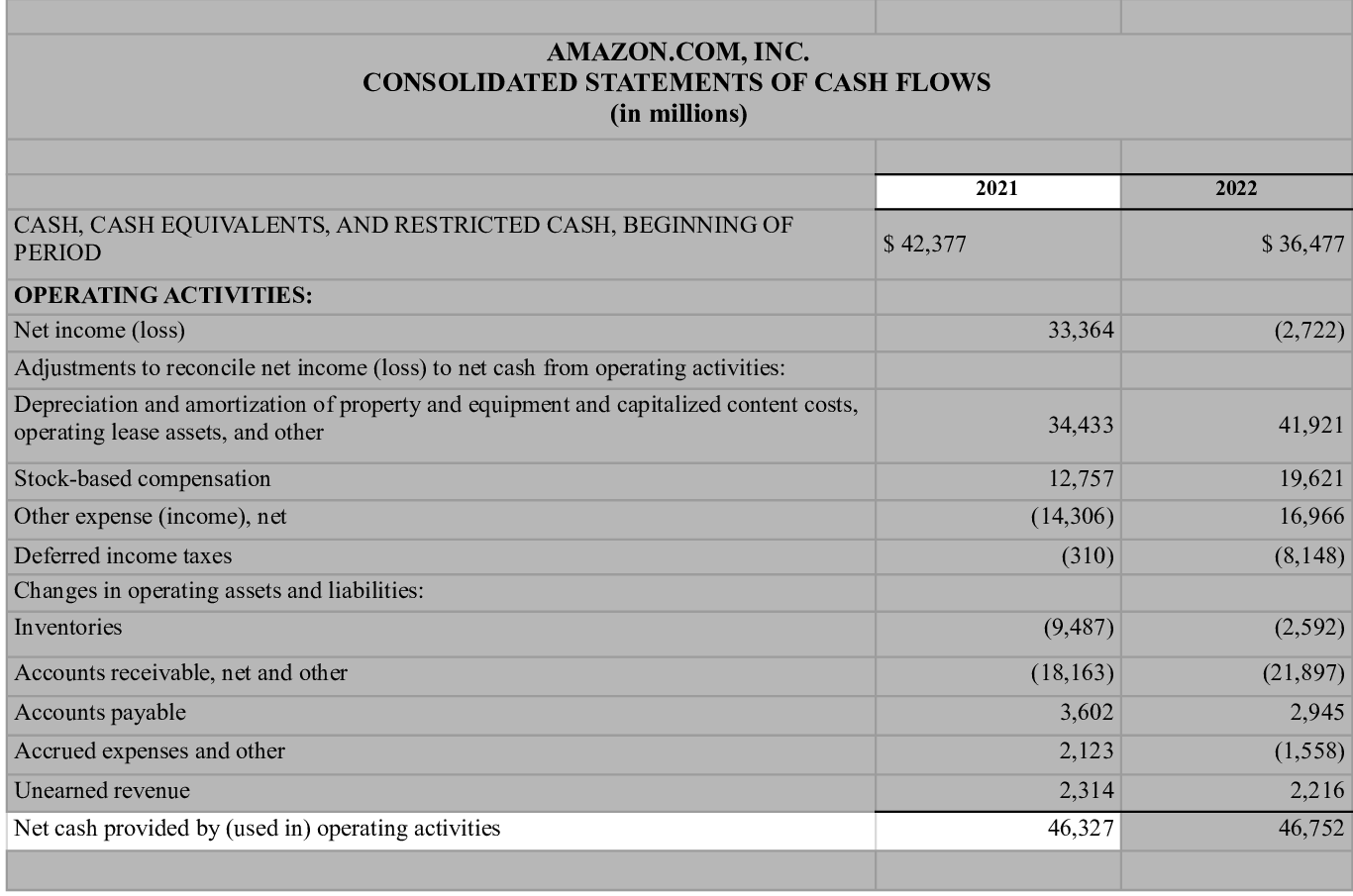

Amazon’s beginning cash and cash equivalent for the year 2022 was $36,477,

which was the closing balance of the year 2021.

Operating Activities

Activities of cash inflow and outflow related to a company’s core business operations are termed operating activities.

For example, Apple’s core business is selling mobile and electronic items,

So manufacturing products and earnings from sales are included in the operating section.

Two methods can be used to calculate operating activities:

- The direct method and

- The indirect method.

We will explore these methods in the next chapter, but here look at the basic information.

Activities directly related to your business’s core operations are included in the direct method.

When using the direct method, the operating section includes:

Cash Inflow:

- Selling products

- Selling services

- Cash collected from customer

Cash Outflow:

- Salary paid to employees

- Cash paid for raw materials

- Bills paid to internet and electricity providers

When you creating a cash flow statement using the indirect method, it includes non-cash transactions and involves items such as:

- Depreciation and amortization

- Income tax expenses

- Accounts receivable

- Net Inventory

- Accounts payable

Most companies prefer the indirect method because it is easier to create.

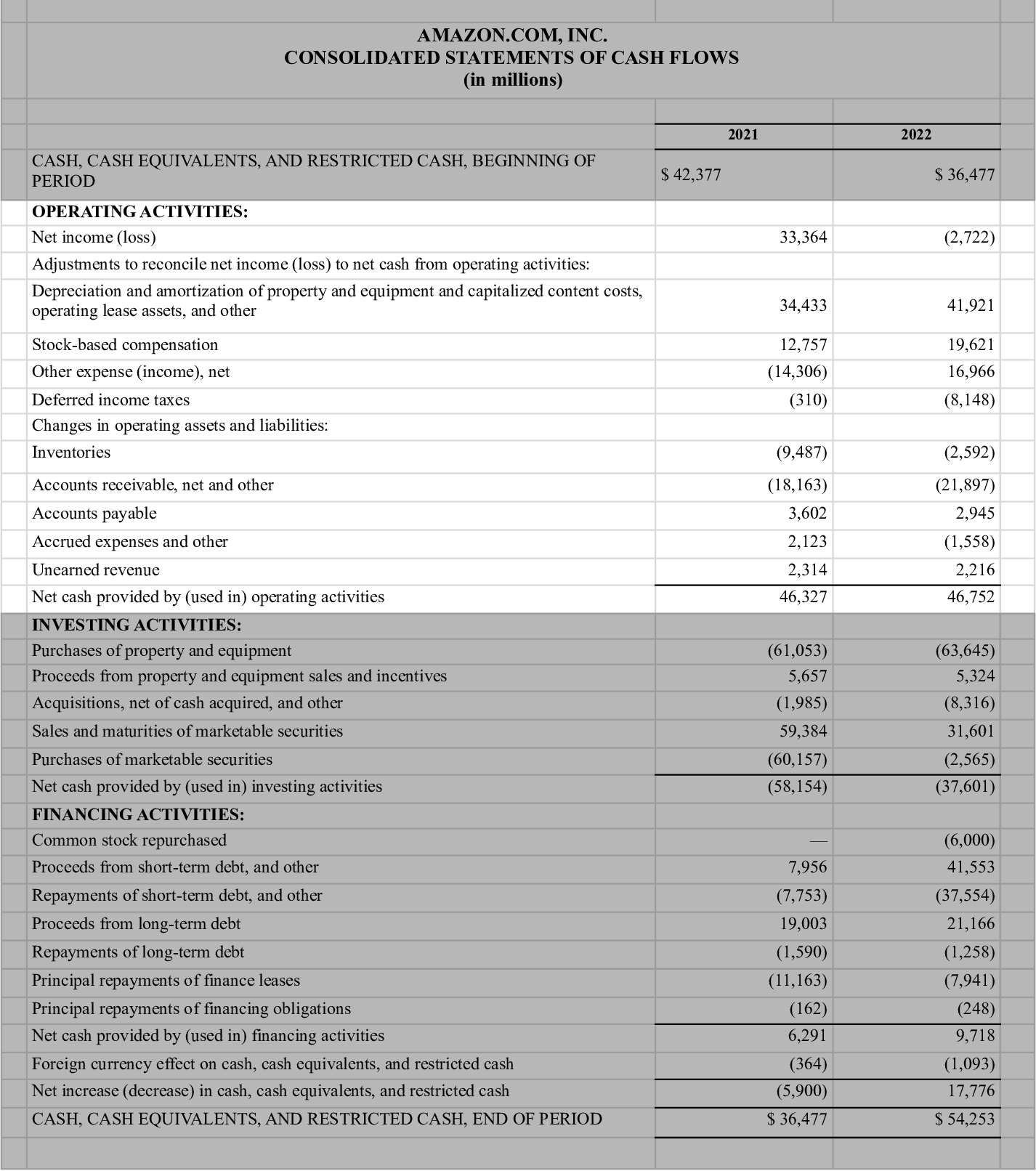

Investing Activities

Cash activities related to a company’s investments are termed investing activities, encompassing the buying or selling of assets.

Generally, firms invest in assets to expand their business. So, investing in long-term assets is categorised in this section.

Here’s a list of investing cash flow.

Cash Inflow:

- Selling property, plant, and equipment (PPE)

- Selling marketable securities

- Selling stocks and bonds

- Selling long-term assets

Cash Outflow:

- Expenditure in property, plant, and equipment (PPE)

- Acquisition of other businesses

- Purchase of marketable securities

- Purchase of stocks and bonds

- Buying long-term assets

Most investing activities involve cash outflows as companies utilize funds to acquire new assets for expansion.

Looking at Apple’s investing activities section,They made substantial investments, such as,

purchasing marketable securities for $34,913M and

earning proceeds from the sales of marketable securities for $10,675M.

Normally, the company’s management team tries to hold cash in a positive way.

But sometimes, firms invest a large amount of money in land, equipment, and assets, which leads to negative cash flow for the current period.

However, it helps the company to grow in the future.

Financial Activities

Financial activities involve activities related to financing the business.

Many organisations require financial help to operate, and these activities are recorded in this section.

For example,

A small business owner providing bread to the local area needs to expand due to high demand.

However, the problem is lacking sufficient cash to purchase land, machinery, and raw materials.

the owner might take a loan as financial help, which would be included in the financial activities section.

Here are Common financial activities:

- Payment for dividends

- Repurchase of stocks

- Repayment of debt

- Bank loans

- Issuing bonds

It’s important to note that interest paid to bondholders is categorised under operating activities rather than financial activities.

Looking at Amazon’s statement,

Cash inflow figures are written without brackets, while cash outflows are enclosed in brackets.

Normally, the net activities of the investing and financial sections are in brackets, which indicates that outflows more than inflows.

This is often because firms are making substantial investments in assets, and some companies may also have significant debt, which leads to high-interest payments and loan repayments.

Final part of the format

We discussed the three types of activities and now it’s time to calculate each of them.

After calculating each activity, the net cash flow is added in the end.

Generally, the operating section concludes as net generating cash, whereas the investing and financial sections are summarised as net used cash.

As we discussed earlier, the main cash source for the company is its core business operations, while most investment and financial activities result in cash outflows.

In the final part of the cash flow statement, the last component indicates the total cash flow from all three business activities:

It Means,

\text{Total Cash Flow} = \text{Operating Cash Flow} + \text{Investing Cash Flow} + \text{Financial Cash Flow}

This total cash flow represents how much cash has increased or decreased during a specific time period, not the actual cash amount.

So the question is, how much cash does the company have at the end?

It is represented by the ending balance And then calculated:

\text{Ending Balance} = \text{Beginning Balance} + \text{Total Increase/Decrease Cash Flow}

This component is represented as “Cash and Cash Equivalents, Ending Balance of the time period” in the sheet.

Remember, The ending balance will become the beginning balance for the next time period when professionals create the statement.

It’s important to note that organisations may add some other components for investors.

For example, Amazon include the effect of foreign currency,

and Apple account for interest paid.

Format of The cash flow statement concludes here.

Chapter 3: Calculate Cash Flow Methods

In this chapter, you will learn how to calculate cash flow.

Especially, You will use two methods:

The direct method and the indirect method.

While both methods impact and change the operating activities section, the investing and financial sections remain the same.

Let’s dive deeper into these methods.

Direct Method

The direct method of the cash flow statement is grounded in the direct transactions of the company.

In this method, receipts from customers and payments for various expenses are categorised.

The direct method is calculated by including all payments made by the company and all sources where cash comes into the company.

Here are the steps to follow when you creating a cash flow statement using the direct method:

Step 1. Identify all payments (cash outflow), such as employee salaries and supplier payments.

Step 2. Identify all receipts (cash inflow), such as product sales and customer payments.

Step 3. Combine both of them to calculate the total cash flow.

The formula is straightforward:

\text{Total Cash Flow} = \text{Cash Inflow} - \text{Cash Outflow}

Many companies use the accrual method for accounting instead of the cash method.

This means they recognize revenue when it’s earned rather than when it’s received.

So what is The key difference?

Almost all the Companies often allow customers to purchase products on credit.

Selling on credit is recognized as sales, but the fact is the company hasn’t received actual cash at that point.

When a company generates revenue by selling a product, it’s considered earned, whether it’s on credit or not.

However, when cash is received in an account, it’s termed as received.

In conclusion, if you assume that all transactions from the income statement will be included in the cash flow statement, you are mistaken.

Therefore, remember that net income (profit) and total cash flow both are different metrics.

Indirect Method

The indirect method begins with net income and adjusts for non-cash items and changes in capital to arrive at net operating cash flow.

Professionals often prefer the indirect method for creating the operating section of the cash flow statement.

Reason is, it is easy to create and less time-consuming compared to the direct method.

Here are the steps to follow when you create a cash flow statement using the indirect method.

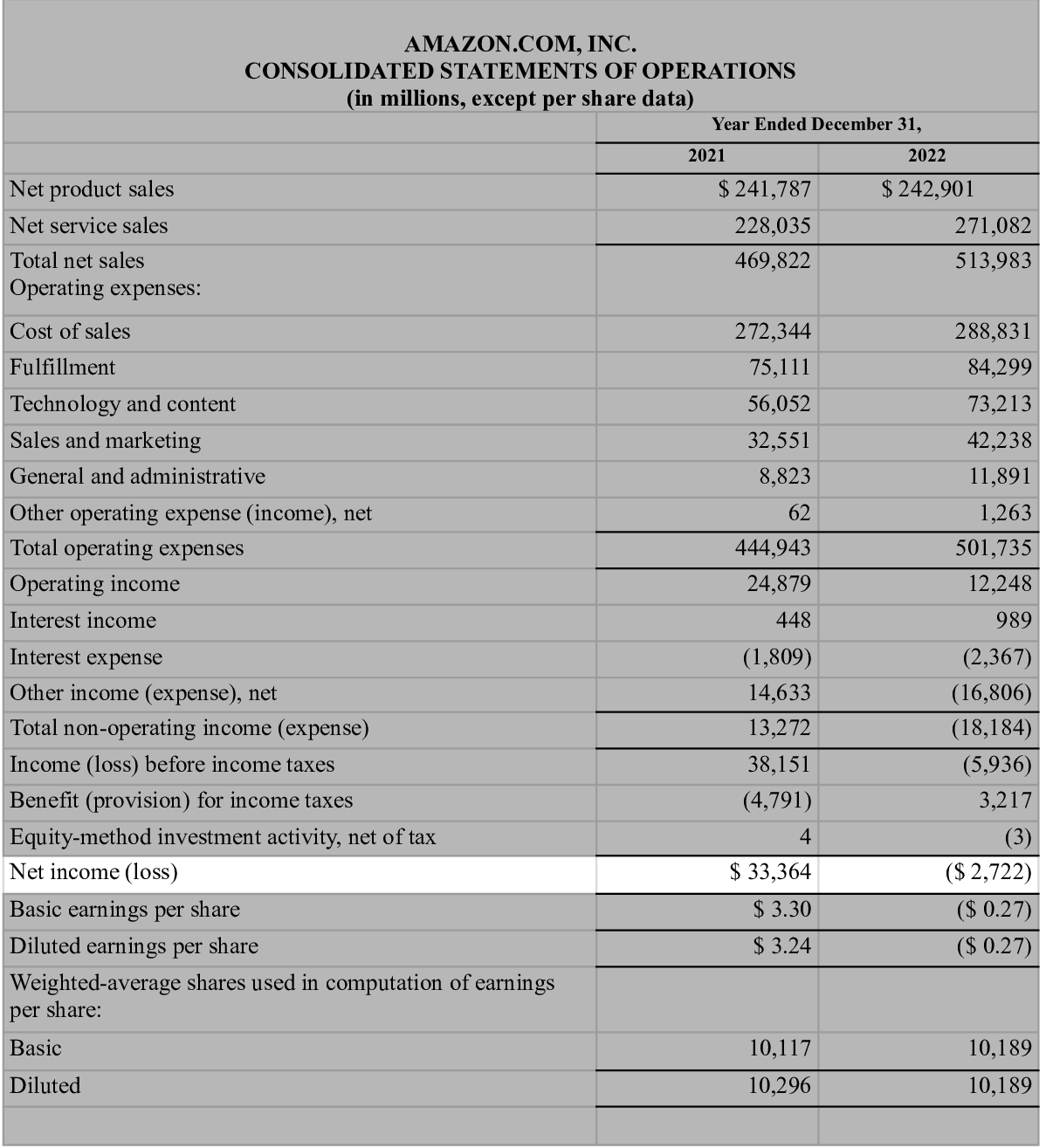

Step 1. Start with net income, which is taken from the income statement.

Step 2. Adjust for non-cash items such as amortization and depreciation.

Step 3. Account for changes in the capital of current assets and liabilities, such as inventory, accounts payable and accounts receivable.

We need the reconciliation for the direct method to connect it with other financial statements, whereas this is done automatically in the indirect method.

Now, let’s move on to the next chapter.

Chapter 4: Cash Flow signals

We discussed what cash flow is and how to create the statement.

The next step is how you will know a company’s financial health using a cash flow statement.

That’s what this chapter is all about.

This chapter will delve into the positive and negative cash flow.

Let’s explore this in detail.

Positive Cash Flow

Positive cash flow occurs when a company earns more from its core business operations than it spends on running the business.

In simple terms, cash inflow is more than cash outflow.

The formula for net cash flow is straightforward:

\text{Net Cash Flow} = \text{Cash Inflow} - \text{Cash Outflow}

When this value is positive, it indicates that the company has positive cash flow.

For example,

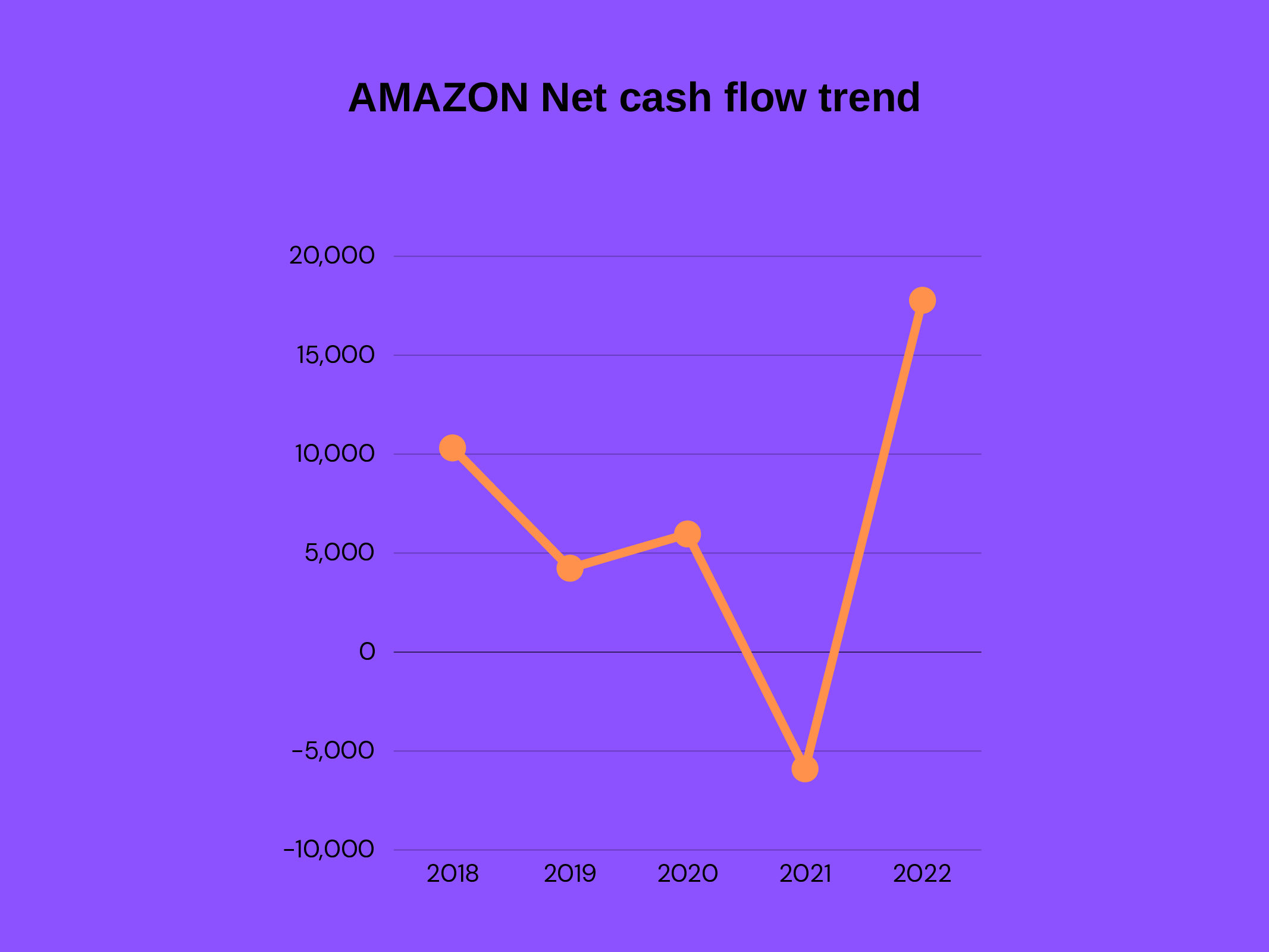

consider Amazon’s total cash flow at the bottom of the sheet.

it’s positive, it means Amazon is earning more than it’s spending.

As an investor, it’s valuable to analyse the trend of cash flow over multiple years. Is it consistently increasing?

Understanding the trend provides deeper insights into the company’s financial health.

You may ask, why is Positive Cash Flow Important?

Positive cash flow brings several benefits:

1. Debt Payout: The organisation can use positive cash flow to pay off its debts.

2. Seizing Opportunities: A company with positive cash flow is better positioned to capture suddenly rising opportunities in the market.

3. Financial Resilience: Positive cash flow helps the organisation withstand financial crises, providing a buffer during challenging times.

However, it’s essential to note that having too much cash on hand may not always be good.

It could suggest that the company is not actively investing money to expand its business or may be avoiding potential growth opportunities.

Negative Cash Flow

Negative cash flow is the opposite of positive cash flow.

Indicating that a company is spending more money than it’s earning.

The formula remains the same:

\text{Net Cash Flow} = \text{Cash Inflow} - \text{Cash Outflow}

In this case, the result should become negative, and this can lead to a cash crisis.

Negative cash flow implies that the company has not sufficient funds to cover its expenses.

Negative cash flow tells us:

1. Debt Repayment: A company with negative cash flow may struggle to pay off its debts.

2. Dividend Payments: There might not be enough cash available to distribute dividends to shareholders.

3. Financial Crisis: Negative cash flow indicates vulnerability in the face of financial crises.

It’s normal for investors to avoid investing in companies that are heading in a negative direction.

But the Negative cash flow often occurs when the performance of the company is not effectively tracked and improved.

It’s important to note that many startups experience negative cash flow initially due to heavy investments in business expansion.

Chapter 5: Role of the Cash Flow Statement

This chapter focuses on understanding how to use the cash flow statement and why it’s important.

Any report is worthless without use.

In this chapter, you’ll discover how the cash flow statement aids internal teams, investors, and banks.

Energising the business

You can create a cash flow statement for your company’s internal team which will help your team to know the actual view of the company’s cash.

The management team or professionals use this financial data to enhance the company’s growth and financial health.

It proves beneficial in various ways:

- Helps in decision-making for future plans.

- Improves cash flow by tracking spending activities.

- Establishes a structure for crisis management.

- Assists in investing in short and long-term plans.

In simple terms,

The cash flow statement, being one of the main financial reports, contains significant data about the organisation.

Without knowing the actual cash position and how much cash is generated from the business, making decisions becomes challenging.

Example for,

If the company has surplus cash, the internal team may choose to invest in Property, Plant, and Equipment (PPE) or pay off debts early.

Tracking cash inflow and outflow helps the team make decisions about where to allocate resources.

If a company faces a low cash reserve or cash crisis, professionals will analyse the statement and decide where to spend and where not to.

For example,

The management team finds out the firm is investing a lot of money in inventory, which is not currently important.

So, they decide to cut the investment in inventory.

Moreover, the cash flow statement provides early warnings about potential future challenges.

Businesses must pay debts on time, including loan interest.

Having enough cash on hand is crucial for timely debt payments.

Here, The cash flow statement alerts professionals in advance and enabling them to take proactive steps.

Enhancing Investor’s strength

Who wants to lose money?

No one. And that’s why the cash flow statement is useful for investors.

How?

It provides the same data to investors as professionals. Both want to check the health of the business, but the intent is different.

Where the management team uses it to make decisions to improve the company.

Investors use this cash flow statement to find out if this firm is worth investing in or not.

As we discussed above, the cash flow statement provides details of spending and generating activities of cash.

If the company is not generating enough cash to pay off its debt, then it’s possible that it will face a financial crisis in the near future.

Which leads to the firm’s valuation going down.

Another aspect is checking the trend of the company.

Comparing the last few years’ net cash flow.

Is it going upward (positive) or declining (negative)?

The next one is analysing the company’s future growth.

You can gain a lot of knowledge just by seeing where the firm is spending.

If a lot of cash goes to paying out loan interest, it means no money will be left for capital expansion.

Also, the company will not be able to give dividends, which also keeps investors away.

Navigate cash flow for Loan

The cash flow statement is crucial when seeking financing for a company, especially when applying for a loan.

Lenders base their decision to approve a loan on the company’s cash flow statement.

For example,

When an organisation approaches a bank for a loan, the bank manager analyses the cash flow statement to assess how much risk is involved in providing the loan.

They check whether the company has generated enough cash to repay the loan.

In essence, they evaluate the credibility of the company using the cash flow statement.

Additionally, lenders may utilise specific cash flow ratios (which we will discuss later) during this assessment.

Furthermore, the cash flow statement holds significant importance for small businesses.

Traditional bank loans typically ask for additional financial reports, such as the balance sheet and income statement.

If you have a large number of assets, you will get a loan easily. However, small businesses may not have enough assets to secure a loan for expanding their operations.

Here, the cash flow statement becomes a saviour.

Many lenders offer loans based solely on the cash flow statement, without matching criteria related to other financial reports.

Lenders just check how much the company generates in cash to approve the loan.

While these loans may have a higher interest rate due to increased risk.

As an example,

OnDeck is a known lender for providing cash flow loans.

The loan amount can go up to $250,000, and the interest rates can range from 20% to 50%.

I suggest you stay away from this type of loan. it will harm your business if you can’t pay the loan on time.

Now, let’s delve into the advanced chapter.

Chapter 6: Cash Flow Ratios

This chapter is all about cash flow ratios.

Ratios serve as a comparison of two or more values from the cash flow statement.

It offers a fast and efficient way to gauge the financial position of the company.

In this chapter, you will learn about three ratios that help in decision-making and provide a snapshot of the company’s current position.

Price to Cash Flow Ratio

The Price to Cash Flow ratio measures a company’s market price per share in comparison to its operating cash flow per share.

In other words, this metric assesses how the company’s market price relates to its operating cash flow.

Formula:

\text{Price to Cash Flow} = \frac{\text{Market Price per Share}}{\text{Operating Cash Flow per Share}}

Alternatively:

\text{Price to Cash Flow} = \frac{\text{Market Price}}{\text{Operating Cash Flow}}

This formula indicates the company’s market value relative to its ability to generate cash from its business.

P/CF is better than Price to Earnings ratio, P/E ratio utilises net income which can be easily manipulated by accounting methods.

Whereas the Price to Cash Flow ratio provides a more accurate position.

Example:

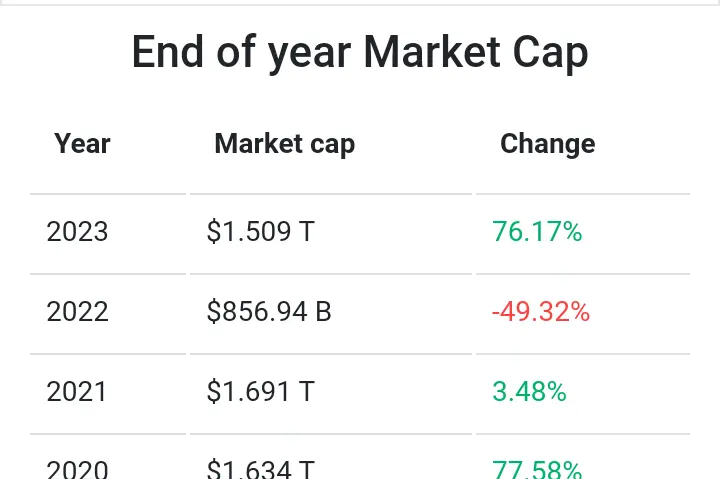

Market Cap Value of Amazon at Year 2021, December = $1.69 trillion

Operating Cash Flow of Amazon = $46.3 billion

By calculating the ratio:

\text{Price to Cash Flow (P/CF)} = 36.5

This indicates that investors are willing to pay $36.5 for every dollar generated from operating cash flow.

Operating Cash Flow Ratio

Operating cash flow ratio measures a company’s ability to use its generated operating cash to cover its short-term liabilities.

In simple terms, this metric compares a company’s operating cash flow to its short-term debt.

Formula:

\text{Operating Cash Flow Ratio} = \frac{\text{Operating Cash Flow}}{\text{Average Current Liabilities}}

Here, liabilities are taken from the balance sheet.

\text{Average Current Liabilities} = \frac{\text{Current Liabilities at the Beginning} + \text{Current Liabilities at the End}}{2}

Example:

Taking the previous example of Amazon,

Operating Cash Flow = $46.3B

Liabilities at the Beginning = $142B

Liabilities at the End = $156B

By calculating the ratio:

\text{Operating Cash Flow Ratio (OCF)} = 0.3\text{OCF (\%)} = 30\%

Here, you can interpret that Amazon is generating cash to cover only 30% of its current debt.

A ratio higher than one is positive, indicating the company can pay its short-term liabilities,

while a ratio lower than one suggests the company may not be generating enough cash to cover its short-term debt.

Cash Flow to Debt Ratio

Cash Flow to Debt Ratio Similar to the OCF Ratio, but it covers both long and short-term liabilities.

This ratio measures the ability of company’s core business-generated cash to pay its total debt.

Formula:

\text{Cash Flow to Debt Ratio} = \frac{\text{Operating Cash Flow}}{\text{Total Debt}}

Total debt includes both long-term and short-term liabilities. And both are found in the balance sheet.

As usual, a higher ratio is a positive signal, while a lower ratio may means professionals to investigate and make improvements.

Conclusion

With this, I conclude my guide and hope you found it helpful.

Now it’s your turn—what is your thoughts on this post?

Are you satisfied with it, or would you like to add something?

Let me know by leaving a comment below right now.