If you find out information about cash flow from operating activities, then you’ve landed on the right page.

Operating cash flow is one of the most important financial sections for internal teams, and investors want to analyse it.

In this post, you will learn what cash flow from operating activities is, how to calculate it, its formula, and real-life examples.

What is cash flow from operating activities

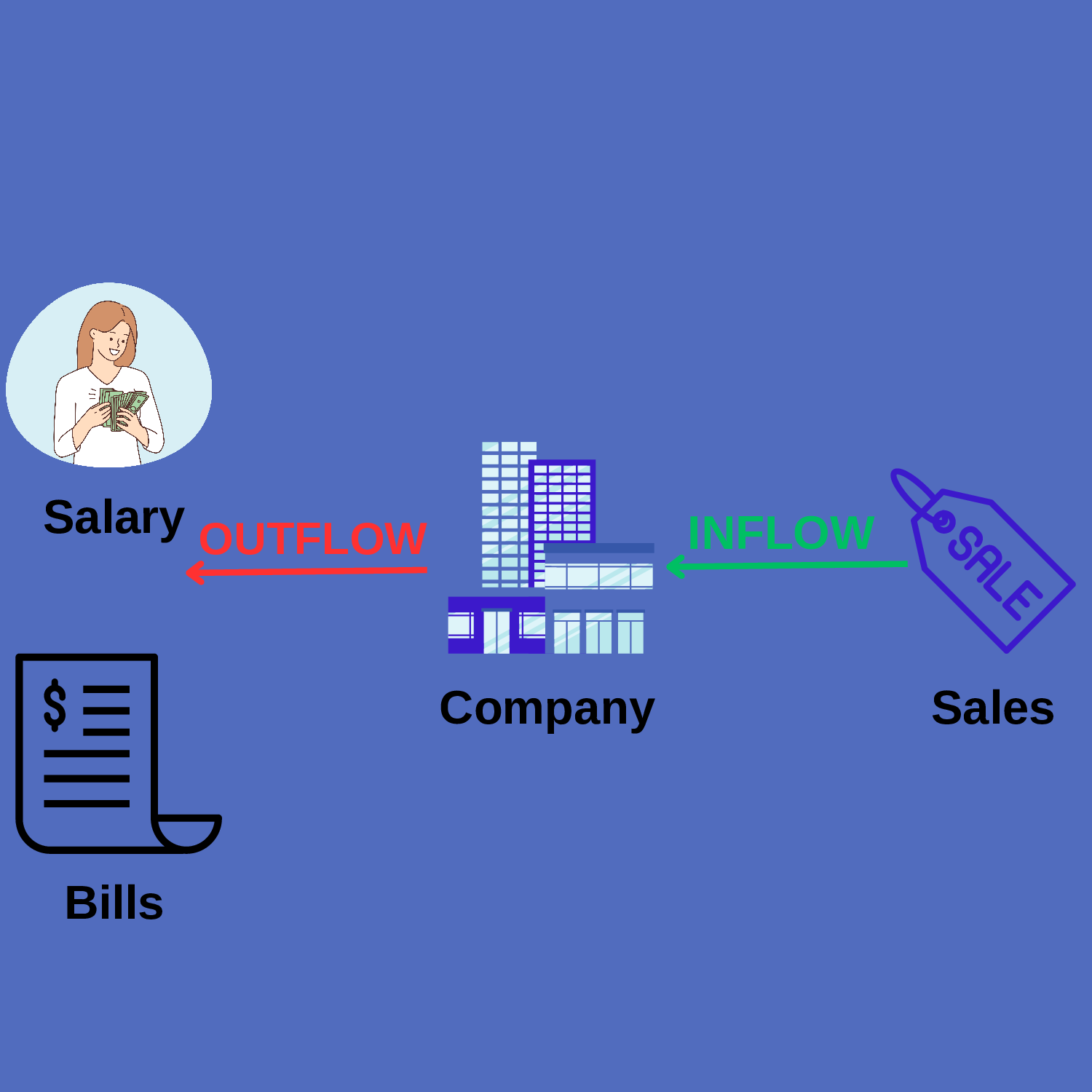

Operating activities are referred to as the activities related to a business’s core operations. Cash inflow and outflow of these activities are referred to as cash flow from operating activities.

Operating cash flow includes all cash flow activities related to a business on a regular basis.

For example, a mobile company’s core business is selling mobile phones. Here, cash coming from the company’s sale of mobile phones and salaries paid to employees for their work are calculated as operating cash flow because they are mainly connected with the company’s core business.

Here is a list of some operating activities:

- Salaries paid to employees

- Cash paid to suppliers

- Cash collected from customers

- Interest income

- Income tax paid

- Accounts receivable

- Amortization and depreciation

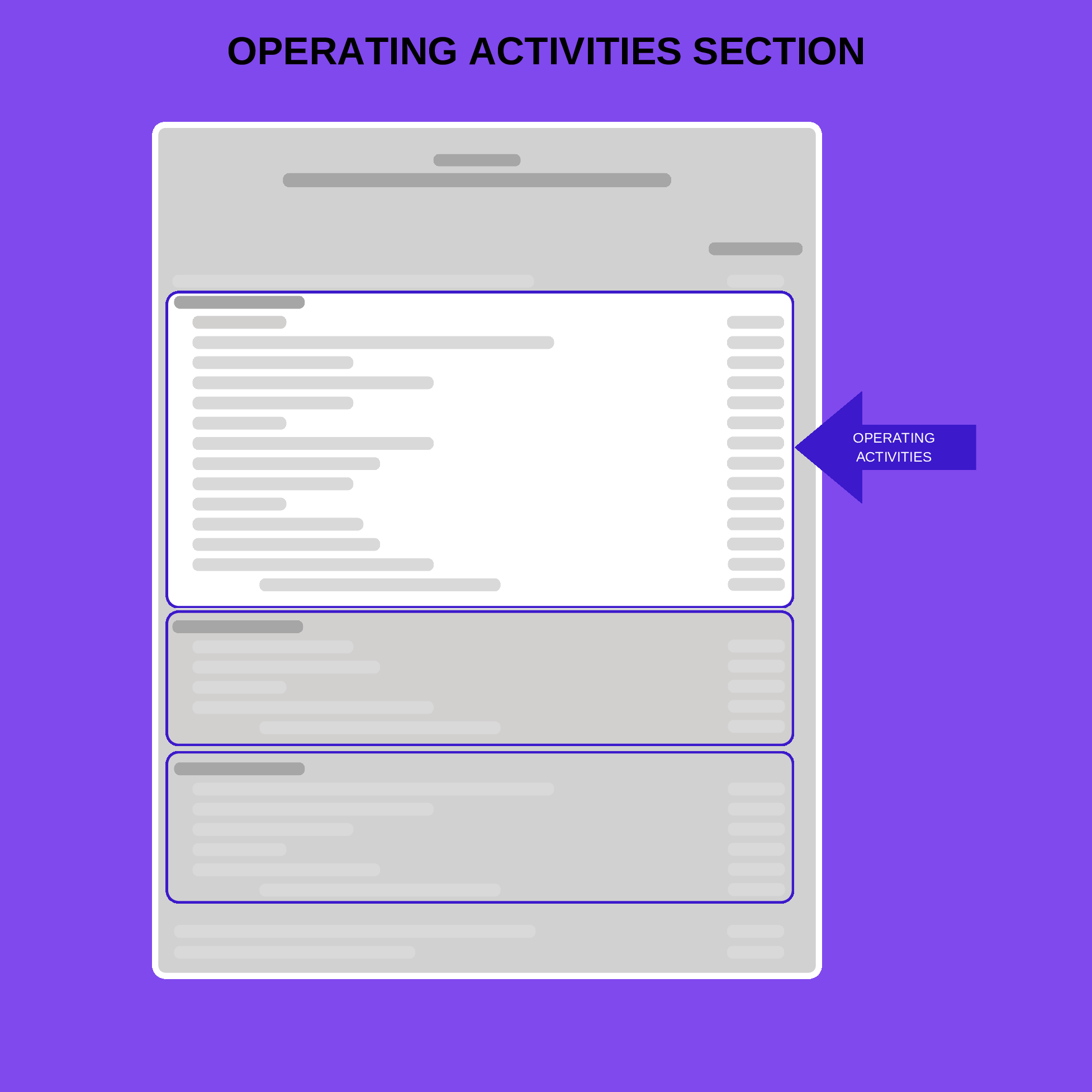

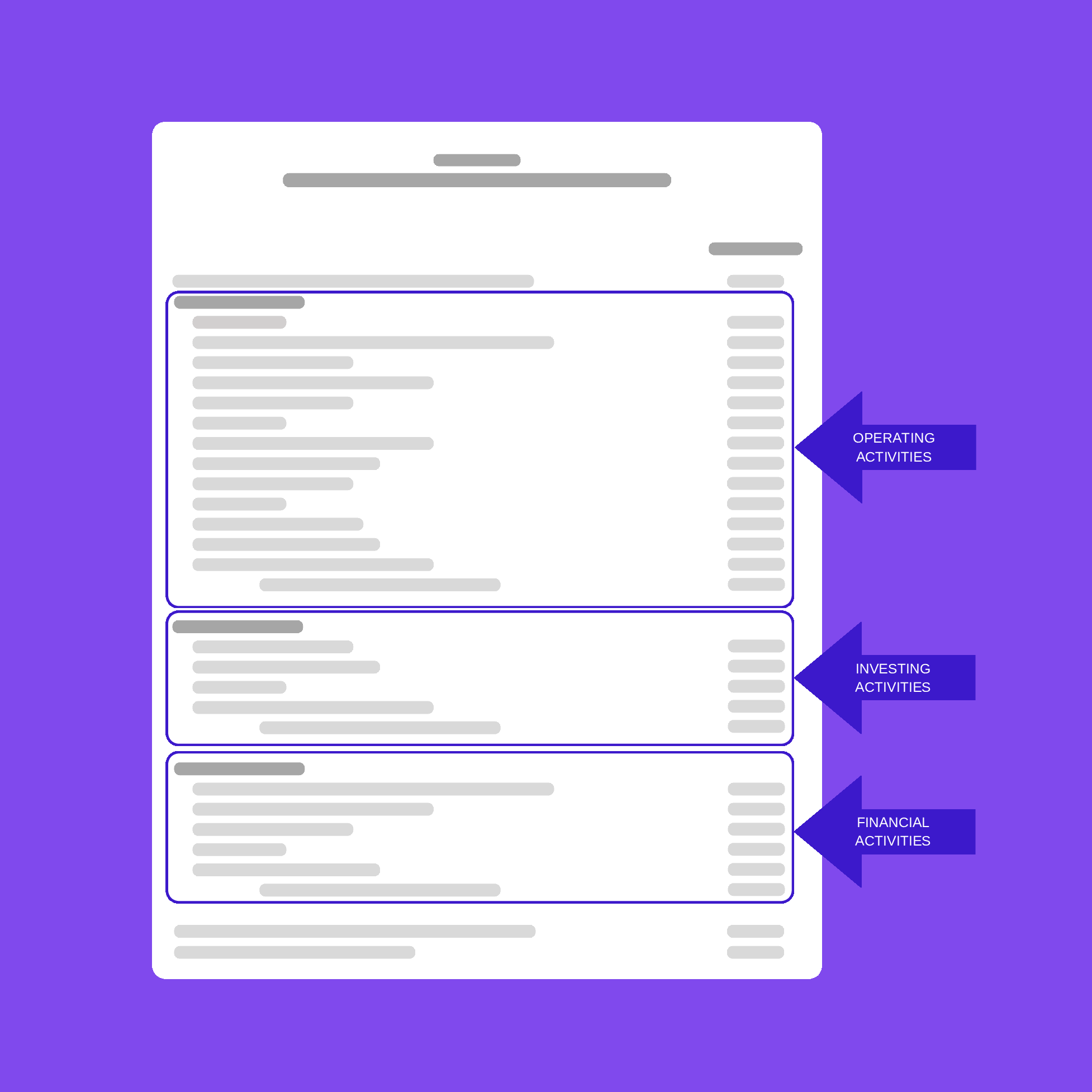

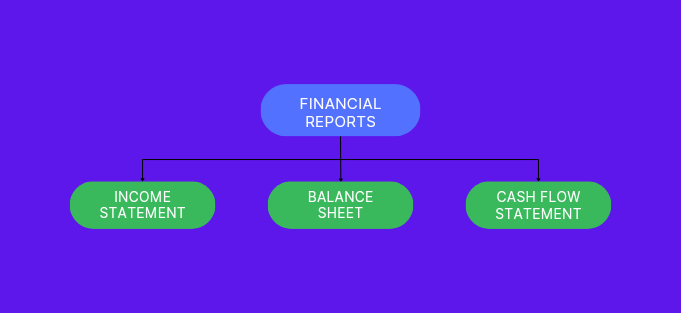

Operating cash flow is part of the cash flow statement, one of the three main financial statements that show the financial position of the company.

The cash flow statement consists of three types of cash flow activities:

- Cash flow from operating activities

- Cash flow from investing activities

- Cash flow from financial activities

Cash flow from the company’s investing activities, such as buying or selling assets, is included in the investing section.

When the company engages in activities related to finance, such as taking loans or repaying loan amounts, they are categorised in the financial activities section.

calculate cash flow from operating activities

When preparing the cash flow statement, you can use two methods for calculating cash flow from operating activities:

- Direct method

- Indirect method

Both investing and financial sections remain the same during both methods. Only the operating cash flow section changes during these two methods.

Direct method

The direct method includes all direct transactions related to business core operations. It includes all sources of cash coming in and going out of the company.

For example, cash coming from selling products is categorised as cash inflow, while paying salaries to employees and bills are categorised as cash outflow.

To calculate cash flow from operating activities using the direct method, follow these steps:

- Find out all receipts: Gather all receipts where cash is coming in, or in other words, make a list of all sources of cash inflow.

- Find out all bills: Gather all bills where the company spent its money. Make a list of cash outflows of the company.

- Combine data: Cash flow from operating activities is divided into two parts: cash inflow and cash outflow. Combine all the above information in one place. First, list all cash inflow activities, and then list cash outflow activities.

- Calculate operating cash flow: Now, calculate operating cash flow using this simple formula:

Operating cash flow = operating cash inflow – operating cash outflow

This will give you the net cash flow from operating activities.

Indirect method

The indirect method starts with net income and arrives at net operating cash flow by adjusting non-cash expenses and net working capital. It takes net income as the base and adjusts other items.

Most companies prefer this method instead of the direct method because it is easier to use.

To calculate cash flow from operating activities using the indirect method, follow these steps:

- Start with net income: The section of operating cash flow starts with net income, which is located in the income statement, also called the profit and loss statement.

- Adjust non-cash items: In the indirect method, you should adjust non-cash expenses such as amortisation and depreciation.

- Adjust net working capital: Now, adjust net working capital, such as inventory, etc.

- Calculate operating cash flow: Now, do the same as in the direct method. Subtract cash outflow from the company’s cash inflow to find out operating cash flow.

Operating cash flow = cash inflow – cash outflow

Alternatively, use the formula:

Net Income + Adjustments to Net Income (non-cash items) + Changes in Working Capital

Since the indirect method starts with net income, it does not need any transparency report, whereas it is necessary for the direct method.

That’s why most professionals prefer the indirect method. However, the direct method is more accurate compared to the indirect method.

Conclusion

In conclusion, cash flow from operating activities is one of the main and important sections of a company to run the business.

It shows where cash is coming into the company and where the company is spending it. However, only knowing operating cash flow is not enough; you should also have an idea about investing and financial activities.

Here are some other amazing articles for you to explore: