Understanding the income statement provides insights into a company’s revenue and expenses. However, it doesn’t offer a complete view of the company’s profitability, as it excludes unrealized income.

The statement of comprehensive income includes both net income from the income statement and other comprehensive income. This combination provides a more accurate representation of the company’s profit.

In this article, we will explore what the statement of comprehensive income is, what it includes, its relationship with other comprehensive income, and provide a real-life example for better understanding.

What is a Comprehensive Income Statement

A Comprehensive Income Statement, also known as the Statement of Comprehensive Income (SCI), offers a broader view of the company’s income. It provides professionals and investors with details about both realised and unrealized earnings.

While the income statement only incorporates earned revenue and expenses, comprehensive income includes both net income and unrealized income from non-owner sources.

Examples of unrealized income include cash flow hedge, derivatives of financial instruments, and gains/losses from foreign currency transactions.

Creating a SCI is not mandatory. Many companies note other comprehensive income as a footnote to their financial statements.

Understanding the Statement of Comprehensive Income

The statement of comprehensive income fulfils its purpose by providing a comprehensive view of the company’s income. It comprises two parts: net income from the income statement and other comprehensive income. Together, these elements form the SCI.

Smaller businesses might not require a comprehensive income statement due to limited unrealized income. However, large companies like Amazon and Apple, operating globally, need it to account for currency fluctuations and significant debt security and investments.

For example, Company ABC invests a substantial amount in debt securities like stocks, bonds, mutual funds, or gold. Although these aren’t recognized as income in the income statement, they are considered unearned income for the company.

Professionals and investors analyse such factors, including debt security and financial instruments, to determine a more accurate financial position of the company.

Generally, other comprehensive income is unrealized and not immediately taxable. However, when the assets are sold, it becomes realised income, and the company incurs taxes. In the above example, when the company sells its bonds, it will be subject to taxation.

Here I provide a basic understanding of what an income statement and other comprehensive income entail.

Income Statement

Net income is located on the income statement and is calculated by subtracting all expenses and taxes from the company’s total revenue.

The income statement is one of the financial statements that companies publish. It generally recognizes earned income from sales and expenses such as the cost of goods sold and tax expenses.

However, it lacks data regarding the company’s other comprehensive income, which is why we need the (SCI).

Other Comprehensive Income

Net income does not provide details about unrealized gains and losses from the company’s assets.

Other comprehensive income includes company income that arises from non-owner activities. Examples include:

- Unrealized gains and losses from company assets

- Gains or losses from pension and other retirement programs

- Unrealized gains or losses from debt securities

- Unrealized gains or losses from available-for-sale securities

- Adjustments made to foreign currency transactions

Note: Other comprehensive income has two types:

1. Operating Comprehensive Income: Related to the company’s core businesses, such as interest and dividends.

2. Investment Comprehensive Income: Not related to operations but associated with investing activities, for example, gains and losses on available-for-sale securities.

Comprehensive Income Statement Example

Not all companies publish the Statement of Comprehensive Income; only those with large-scale businesses and unrealized income or loss typically do.

The Statement of Comprehensive Income format is almost similar to the income statement. The key difference is that it includes both net income and comprehensive income. Here is a sample format for the Comprehensive Income Statement:

Company Name | |

Statement of Comprehensive Income (SCI) | |

| Amount | |

| Net income | |

| Other Comprehensive Income | |

| Unrealized Gains/Losses | |

| Foreign Currency Adjustments | |

| Total Other Comprehensive Income | |

| Comprehensive income | |

It is categorised into two parts: the first one is net income, and the second one is other comprehensive income.

Look at the Components of Other Comprehensive Income.

1. Available-for-Sale Securities: Companies hold securities for an extended period.

2. Financial Investments: Companies invest in various assets like stocks, bonds, gold, and real estate.

3. Retirement Plans: Many companies invest in pension and retirement plans.

4. Debt Security: It is a financial instrument in which a company invests, paying back the principal amount and interest. An example is a government bond.

5. Foreign Currency Transactions: Gains and losses from currency transactions are typically not mentioned on the income statement, hence included in other comprehensive income.

Many companies add other comprehensive income data to the income statement, noted as a footnote.

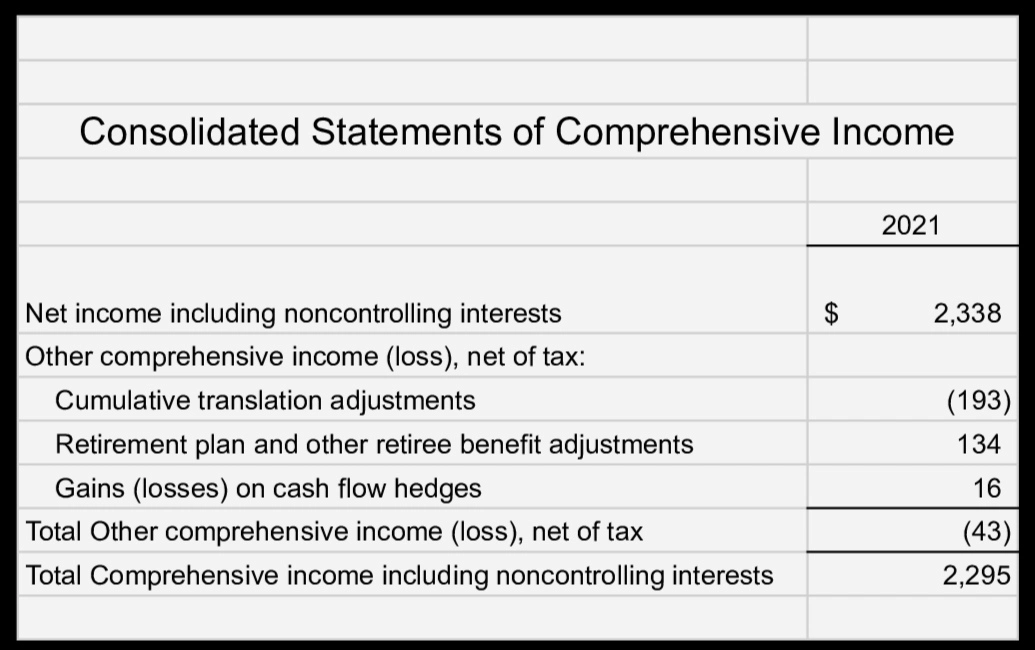

Example 1: colgate Company

Here is Colgate Company’s Statement of Comprehensive Income.

This example includes net income from the income statement and various components of other comprehensive income.

at the end, the sum of net income and OCI to obtain comprehensive income.

Example 2: Cris’s Shoe Shop

Cris, a small business owner, earned good money from his shop and invested $1000, in an oil company named Reliance. Initially, this invested money doesn’t reflect in the income statement because it is unearned income.

However, when Cris sells the shares, it becomes earned income and is added to the income statement.

Income Statement vs. Statement of Comprehensive Income

It is necessary for you to understand the difference between the income statement and the statement of comprehensive income (SCI).

The income statement provides a view of a company’s main revenue and expenses. Starting from revenue and subtracting all expenses to get net income, it does not include any unrealized gains and losses.

On the other hand, the SCI provides both realised and unrealized gain and loss data. It includes other comprehensive income and net income for a broader view.

Benefits of the SCI

Generally, management teams and investors look at the income statement to assess the profitability of the company. However, having a comprehensive income statement is a better idea.

For Management Teams: The statement of comprehensive income is used by internal teams to understand how profitable and stable the company is.

Using this data, professionals in the company can make better decisions and create more accurate plans for the future.

For Investors: Investors’ main priority is investing in a company with a good return.

While the income statement provides details of realised income and expenses, the comprehensive income statement provides more income data that helps investors have a more accurate understanding of the company, aiding in decision-making.

Investors use this statement, along with other financial statements, to find out financial ratios like earnings per share, indicating how profitable the company is.

FAQs

1. What is in a Comprehensive Income Statement?

Net income and unrealized income are both elements in the Comprehensive Income Statement.

2. What are the two statements of Comprehensive Income?

The two statements are the income statement and the other comprehensive income statement.

3. What is the purpose of reporting comprehensive income?

The main purpose of reporting Ci is to reflect unrealized income to measure the actual income of the company.

Conclusion

In summary, having a Statement of Comprehensive Income is beneficial for businesses, providing essential information for both management teams and investors.

However, relying solely on income-based statements may not be ideal for assessing a company’s financial position.

It is crucial that you have knowledge regarding the company’s cash flow and its statement. Here I refer to my comprehensive guide on cash flow statements. It will undoubtedly increase your financial knowledge significantly.

Suggested Article: Cash Flow Statement: Definitive Guide