In this post, you will learn everything related to the classified balance sheet, including what it is, how to prepare it, format, and example.

Many professionals use this method to obtain more comprehensive information related to their business.

Here you will learn how to prepare a classified balance sheet with examples.

So let’s start.

What is a classified balance sheet

Classified balance sheets contain more information and are divided into more subcategories than traditional balance sheets.

While the traditional balance sheet includes assets, liabilities, and shareholders’ equity, the classified balance sheet divides these parts into other subcategories. A classified balance sheet is more informative and provides a comprehensive view.

Format of Classified Balance Sheet

To understand the classified balance sheet in detail, you need to comprehend its format. Although its format is not much different from a traditional sheet, it just has more subsections of elements and is a little more complex.

The general balance sheet includes three main parts of a company’s elements: assets, liabilities, and shareholders’ equity.

The company has a variety of assets and liabilities. The classified balance sheet describes these types and includes them in their respective categories. It is not fixed how many subcategories the sheet should have; professionals can adjust as per their requirement.

Here we will explore the general format of the sheet and briefly go through all the sections.

Assets

Assets are things that the company owns. This can be anything over which the company has rights. Examples are cash on account, assets, and inventory. The assets are divided into three subcategories.

Short-term assets: These assets can be converted into cash within a year. Raw materials, inventory, and cash at banks are considered in this subcategory.

Long-term assets: Assets which cannot be converted into cash within the year are categorised as long-term assets. Land, equipment, and bonds are examples of long-term assets.

Intangible Assets: These assets are not physical but still have value in the company. Examples such as brand names, patents, and trademarks are categorised in this section.

Liabilities

Liabilities are obligations the company owes. Whatever the company owes is classified in this section. Liabilities are also classified into two subcategories.

Short-term Liabilities: These liabilities, which the company has to repay within a year, are called short-term liabilities. Accounts payable and short-term loans are the components classified in this section.

Long-term Liabilities: These liabilities, which the company has to repay after one year or in the next few years, are included in long-term liabilities. Bank loans are a prime example of it.

Shareholders’ Equity

Equity is whatever is left after subtracting all liabilities from assets. In other words, the owner’s equity is what the owner has left after paying all liabilities.

This subcategory includes retained earnings and capital stock. Shareholders’ equity is always shown along with the liabilities section. But in a classified balance sheet, you can show it separately.

The golden rule of any balance sheet is that the value of assets is always equal to liabilities and shareholders’ equity.

Assets = Liabilities + Shareholders’ Equity

How to Prepare a Classified Balance Sheet

Preparing a classified balance sheet is easy when you do it step by step. However, you have the option of creating classified balance sheets using software. Here we will prepare a classified balance sheet manually.

1. Download Template

Create a balance sheet template in Excel. For our readers, there is no need to start from scratch. Download the given template and adjust it as per your requirement.

The first row of the template includes a variety of elements such as accounts payable, inventory, etc.

The figures of the elements are mentioned on the front side. Some elements may differ for different companies. Adjust as per your needs.

2. Find All assets

List all assets including current assets, long-term assets, and other assets. After collecting all the assets, calculate the total assets. Use this simple formula:

Net Assets = Current Assets + Long-term Assets + Other Assets

It will be helpful to look at the traditional balance sheet and other financial statements such as cash flow statements and income statements to locate all of the company’s assets.

3. Find All Liabilities

List all liabilities, including current and long-term liabilities. Similar to assets, data can be found in financial statements. After making the list, total both short-term and long-term liabilities.

This is the formula:

Total Liabilities = Current Liabilities + Long-term Liabilities

4. Add Shareholders’ Equity

For shareholders’ equity, you have two options: either create a new section with all the shareholders’ equity elements or add it to the liabilities section.

List all components of shareholders’ equity such as issued stock and retained earnings. Then add the total value of shareholders’ equity along with the liabilities.

Here is the formula:

Liabilities and Shareholders’ Equity = Liabilities + Shareholders’ Equity

5. Check Calculation Sheet

After listing the assets, liabilities, and equity, double-check all the data to verify and ensure it is error-free. Check whether the assets figure is the same as the liabilities and shareholders’ equity.

If not, then you have made a mistake somewhere in the sheet. As we discussed, assets should equal the value of both shareholders’ equity and liabilities.

Example of a Classified Balance Sheet

Let’s take the example of the hypothetical company XYZ here. This way, we can better understand the classified balance sheet.

Here is the assets section of the company, which is divided into three parts: current assets, non-current assets, and fixed assets.

The value of all these types of assets is $525,000.

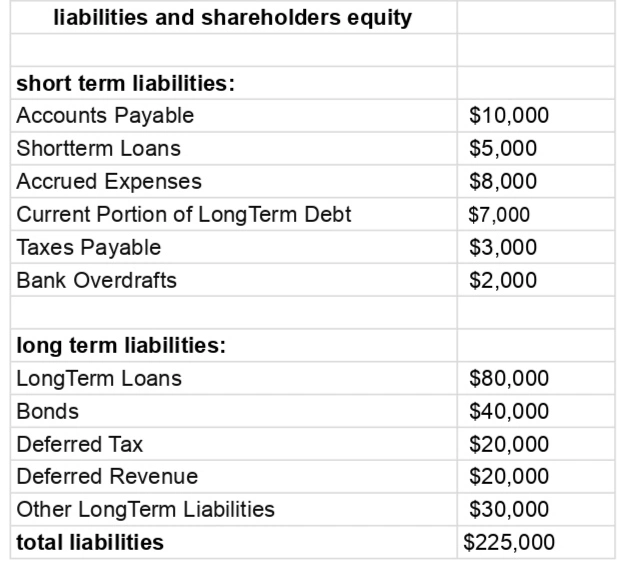

Next is the liability section. The company has entered all the liabilities, including short-term and long-term, in an Excel sheet.

The company’s total liabilities are $225,000.

In the last section, shareholders’ equity is added to the liabilities and shareholders’ equity section.

The total shareholders’ equity value is $300,000.

Now compare assets with liabilities and shareholders’ equity.

The value of total assets is $525,000, and the sum of liabilities and shareholders’ equity is also $525,000.

Conclusion

Before concluding the article, here are three main points I summarised:

The classified balance sheet is a more detailed version of the traditional balance sheet. It has many subcategories unlike a traditional sheet.

Assets have three subcategories (current, fixed, and intangible), while liabilities have two subcategories (short-term and long-term) plus an owner’s equity section.

Always use a template to create a classified balance sheet; it makes the work easier and does not waste time.

Now, I will end my guide. I hope you liked it.

Are you ready to create your company’s classified balance sheet?

Now comment the name of the your company.